Most homeowners think they can “wing it” for remodeling, assuming that a little bit of extra cash tucked away in a savings account will cover the inevitable surprises of a kitchen gutting or a basement finish. They are wrong. A renovation project is not a controlled experiment; it is a financial minefield where the cost of labor, materials, and unexpected structural decay can spiral out of control before the first tile is even laid.

If you want to actually finish a project rather than just starting a series of expensive, half-completed disasters, you need to stop treating home improvement like a hobby. It is a capital investment. Treating it like a casual expense is the fastest way to find yourself living in a construction zone for the next three years while your bank account bleeds out.

We have seen too many people attempt to fund these upgrades through high-interest credit cards or, worse, by simply “making it work” month-to-month. This approach is a recipe for disaster. When the plumbing behind that old drywall turns out to be rusted iron instead of copper, the “making it work” strategy collapses immediately. You need a defined, structured way to access capital before the hammer even hits a nail.

The reality is that financing is not a sign of failure; it is a tool for precision. When used correctly, it allows you to lock in material prices and labor contracts today, rather than waiting until next year when inflation has pushed the cost of lumber or granite another 15% higher. It turns a chaotic series of payments into a predictable monthly obligation.

The Debt Hierarchy: Choosing Your Financial Weapon

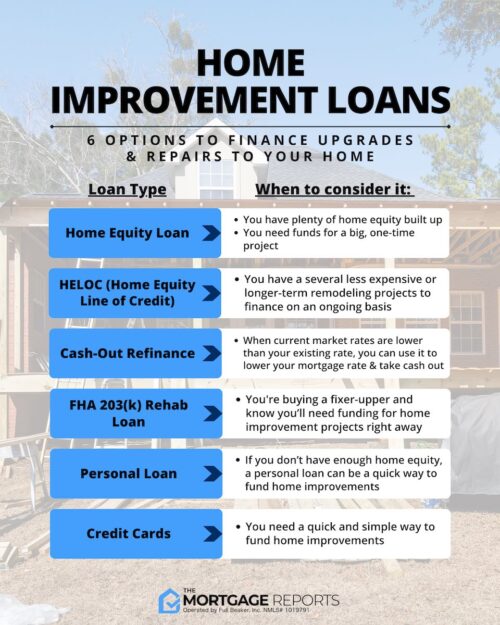

Not all debt is created equal, and choosing the wrong type of financing for a renovation can be more expensive than the renovation itself. People often jump straight to home equity lines of credit because the interest rates look low, but they forget that they are putting their roof on the line. If a contractor disappears or a project goes sideways, you are still on the hook for that house.

Unsecured personal loans have become the dominant choice for mid-sized projects. They don’t require you to put your home up as collateral, which provides a layer of protection if things go wrong. However, the trade-off is usually a slightly higher interest rate. It is a balancing act between risk and cost that every homeowner must navigate carefully.

If you are looking at the US market, you have several distinct paths. You might look at a traditional bank, or you might look at specialized lenders. For example, LightStream is often cited as a top choice for larger, pricier projects, offering personal loans of up to $100,000 for those who qualify. This is a significant jump from the small, quick-fix loans offered by many retail credit providers.

Then there are the credit cards. They are useful for small, immediate needs, like buying a new faucet or a box of high-end screws, but using them to fund a full bathroom remodel is a financial death wish. The interest rates on most cards will eat your equity alive. You need to match the scale of the debt to the scale of the work.

- Credit Cards: Best for small, immediate repairs or material pickups. High interest risk.

- Personal Loans: Fixed rates and predictable terms. Best for medium to large renovations.

- Home Equity (HELOC/Loans): Lowest rates but puts your property at risk. Best for massive, structural overhauls.

Is your credit score actually ready for this? Most lenders won’t even look at your application if your score is in the basement, meaning your “low rate” dream will vanish before you even get a quote.

Navigating International Markets and Local Nuances

The landscape of borrowing changes significantly depending on where you are standing. If you are looking at the European market, specifically the Netherlands, the options and the regulatory environment feel quite different from the American consumer credit model. Banks there tend to have very streamlined, digital-first approaches to personal lending.

Take ABN AMRO, for instance. They offer a highly-rated lending product for those in the Netherlands, with a rating of 8.9/10 from a significant number of users. One of the major advantages they highlight is the ability to calculate a loan in under two minutes and the fact that there are no fees for additional repayments. This flexibility is vital because, as we have established, renovation costs are rarely static.

When you can pay off a chunk of a loan early without being penalized, you have a massive advantage if you suddenly come into extra cash or find that the project was slightly cheaper than anticipated. This flexibility is a luxury that many high-interest “quick cash” lenders simply do not provide. It changes the math of the entire project.

Then you have ING, which provides specific personal loan products tailored for renovation goals. They encourage users to make a calculation of the costs first to get a personal quote. This data-driven approach is much healthier than the “guess and check” method many homeowners use. Whether you are in Amsterdam or Austin, the principle remains: calculate before you commit.

| Lender Type | Primary Benefit | Primary Risk |

|---|---|---|

| Traditional Banks | High stability and established reputation | Slower approval processes |

| Online Lenders | Speed and digital ease of use | Potentially higher rates for lower scores |

| Specialized FinTech | Tailored for specific project needs | Less brand recognition |

If you are looking for more localized options or perhaps need to bridge a gap in a specific region, checking out resources like texasloanstoday.com might provide a different perspective on regional lending trends and availability.

The Hidden Math of Interest and Terms

The number you see on the advertisement is rarely the number you end up paying. This is where people get tripped up. You see an interest rate of 6.74% and think you are in the clear, but you haven’t looked at the term length or the origination fees. A low rate over 7 years might actually cost you more in total interest than a higher rate over 3 years.

Wells Fargo is a classic example of a major player in this space, offering unsecured home improvement personal loans with rates starting as low as 6.74%. This is an attractive entry point, but you must look at the fine print. Are there fees for applying? Are there fees for paying the loan off early? Do the rates change if you don’t meet certain criteria during the underwriting process?

We have seen many homeowners get stuck in a “term trap.” They take a long-term loan to make the monthly payment look small and manageable. They feel a sense of relief when they see a low monthly bill. However, they fail to realize that they are essentially paying for their kitchen in slow motion, paying interest for years on something that has already depreciated in value.

Always prioritize the total cost of the loan over the monthly payment. If a lender offers you a lower monthly payment, ask them exactly how much more you will pay in total interest over the life of that loan. The answer will often surprise you. It is better to struggle slightly with a higher monthly payment now than to pay for a new floor for the next decade.

Avoid the “minimum payment” mentality. If your loan allows for extra repayments without a penalty, use every spare dollar you find to chip away at the principal. This is the only way to truly win the game of interest.

Avoiding the Contractor Trap and Funding Pitfalls

Even with the best loan in the world, you can still lose money if your funding strategy doesn’t match your contractor’s payment schedule. Many contractors want a large deposit upfront. Some lenders won’t release the funds until the work is completed or milestones are met. This creates a massive cash flow gap that can leave you stuck in the middle of a renovation with no way to pay the people doing the work.

You must align your loan disbursement with your project’s milestones. If you are using a personal loan, you usually get the lump sum upfront. This gives you the power, but it also gives you the responsibility of managing that cash. If you spend the money on a high-end backsplash before the subfloor is even replaced, you have effectively sabotaged your own project.

There is a specific way to handle this:

- Milestone 1: Demolition and debris removal (30% of budget).

- Milestone 2: Rough-in plumbing and electrical (30% of budget).

- Milestone 3: Drywall and flooring (25% of budget).

- Milestone 4: Finishing touches and inspection (15% of budget).

Always include a 15% to 20% buffer in your loan amount. If you think the bathroom will cost $10,000, you should be applying for $12,000. That extra $2,000 isn’t “extra money”; it is an insurance policy against the inevitable discovery of mold, rot, or outdated wiring that sits behind your existing walls.

If you don’t have that buffer, you are not planning; you are gambling. A renovation without a contingency fund is just a very expensive way to stress yourself out. Get the loan, get the buffer, and get the work done right the first time. For the full picture, it’s worth checking texasloanstoday.com.

Common questions

Can I use a personal loan for home improvements?

Yes, personal loans are unsecured funds that can be used for any purpose, including renovations, landscaping, or repairs.

Is a personal loan better than a home equity loan for remodeling?

Personal loans offer faster funding and easier approval, while home equity loans typically provide lower interest rates but require your property as collateral.

Will a personal loan for home improvement affect my credit score?

Applying for a loan may cause a temporary dip due to a hard inquiry, but consistent on-time repayments can improve your credit score over time.

How much can I borrow for home renovation via a personal loan?

Loan amounts typically range from $1,000 to $50,000, depending on your creditworthiness and the lender's specific policies.

What are the main advantages of using a personal loan for repairs?

Personal loans provide quick access to cash without using your home as collateral, making them ideal for smaller or urgent projects.